Sky's Adam Parsons reports.

Monday, 29 June 2020

French fisherman fear losing access to British waters in Brexit talks.

He could probably catch fish in the bath!

As the Twilight III manoeuvres into a berth alongside the fish market in Newlyn...

on deck, the attention of Rockets and Sheriff is caught by the sight of a certain Cod aboard his punt Butts with his bass poles deployed in the harbour...

making another sweep past them...

Cod holds up a decent sized bass! - the results of fishing in the harbour produced two fish - a first for the port's top bass man!

Sunday, 28 June 2020

Weekend action in Newlyn.

Resurgan makes her way in through the gaps...

she is now one of six currently in service fishing from the company that once boasted being the largest privately owned fishing fleet in Europe...

looks like someone found a missing trawl door...

while the Cornsh sardine fleet wait patiently on their pontoon berths...

there's still plenty of work to be done on the quayside preparing their ring nets...

special berth...

to repair her worn sides...

Bon Accord the latest crabber to join the Rowse fleet with a stash of pots waiting on the quay to be deployed...

along with several hundred more pots...

stacked five high further up the quay...

Brixham registered stern trawler Angelina taking time out in Newlyn, wouldn't take much of a sea to get your boots wet aboard her...

another visiting trawler, the 10m FY33 Caralee from Fowey

young Roger Nowell downsized from his last vessel the Imogen III to the very tidy looking ex-Brixham trawler Eloise...

Brixham provides yet another visitor in the shape of the

KCJ Rose, currently rigged for stern trawling...

never a good sign to see one of the big beam trawlers with heavy weights in the side deck...

normally an indication that they will be against the quayside for some time...

who knows what thew future of the Lisa Jacqueline will bring...

tidy scalloper working deck.

Saturday, 27 June 2020

The food frontline: Richard Adams, fishmonger

The South West food and drink industry has been severely hit by lockdown as restaurants have closed and producers have lost their customers. Yet some businesses are experiencing an unprecedented boom, while others are pivoting in new and creative directions.

We spoke to foodies on the frontline about what’s been going down.

Richard Adams works in his family business Trelawney Fish & Deli in Newlyn, Cornwall, alongside his brother Anthony and shop manager Andy Howes. In addition to their fish shop in the town, they also provide an overnight fresh fish mail order service for consumers and supply wholesalers that stock restaurants and small fishmongers across the UK.

How has lockdown affected your business?

We’ve seen a massive increase in demand for our overnight delivery service. I think it’s because people can’t go out to restaurants and are looking to treat themselves – plus they’re doing more cooking at home.

On the other side, there’s been a huge decrease in wholesale orders, so the direct to- consumer trade is helping us keep people employed. The wholesale business is starting to stabilise though; we’re now selling more fish to wholesalers that supply small fishmongers. People are getting used to the new normal and are using their local fishmonger more.

How have you adapted?

Our shop is still open but we can only have one customer in at a time. The biggest change is that the mail order element was just an add-on to the business, but we’ve now got a member of staff working on just that – and they’re flat out. We’ve even got a backlog of orders. Other businesses offer a set-price box and customers get what they’re given but we offer a bespoke service where people order over the phone and we advise on what’s best that day, so it’s time consuming.

Has the local community been supportive?

Definitely – the shop counter is still busy. The only thing we’re seeing a dip in is tourist trade.

What will you do after lockdown?

We’ll aim to maintain the level of overnight deliveries we’re doing. A lot of places in the country don’t have a fishmonger and many people didn’t know they could order fish by mail so I hope that after they’ve seen how good the quality, service and the price is, they’ll carry on ordering this way.

People may just return to their usual habits, but if we could do even 50 per cent of what we’re doing now, it would be good. It’s better for people to support fishmongers than supermarkets as fishmongers have more interest in the fishing industry – instead of just the bottom line.

Friday, 26 June 2020

The Lowlife of British fisheries

By Neil Stratton

THIS ARTICLE, the third in a series that considers – how fish landings might look if the major fleets fishing in the NE Atlantic landed a share of the overall harvest that matched the share taken from the corresponding EEZ – examines five species of flatfish: Plaice, Lemon Sole, Common Sole, Turbot and Megrims (strictly speaking, Megrims is a genus).

The first article included general notes about data sources, methodology and the caveat that the following analyses do not assume any particular form of fisheries agreement but merely provide an indication of how shares would change if such an agreement or agreements matched give to take. These continue to apply.

So, without further ado let’s start with Plaice.

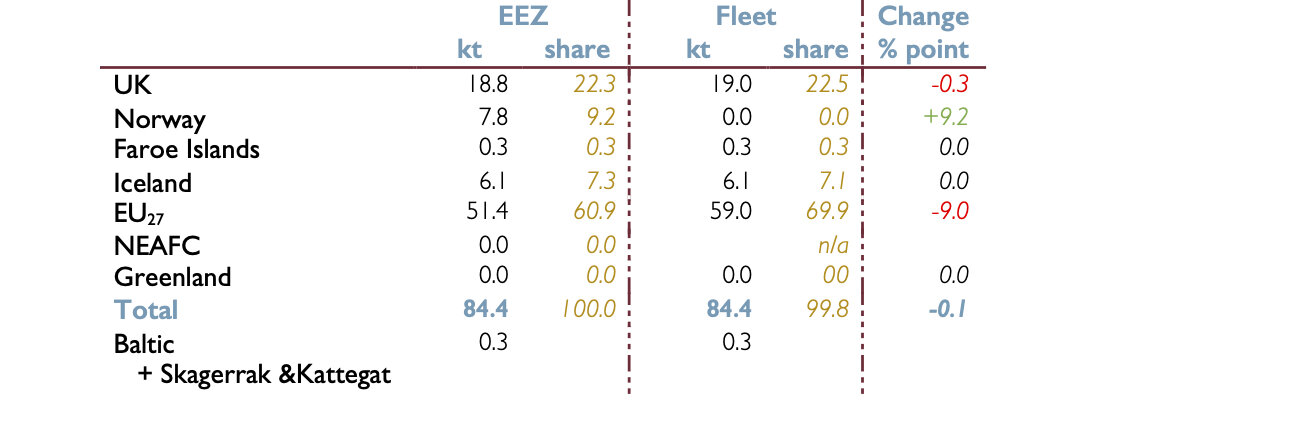

PLAICE

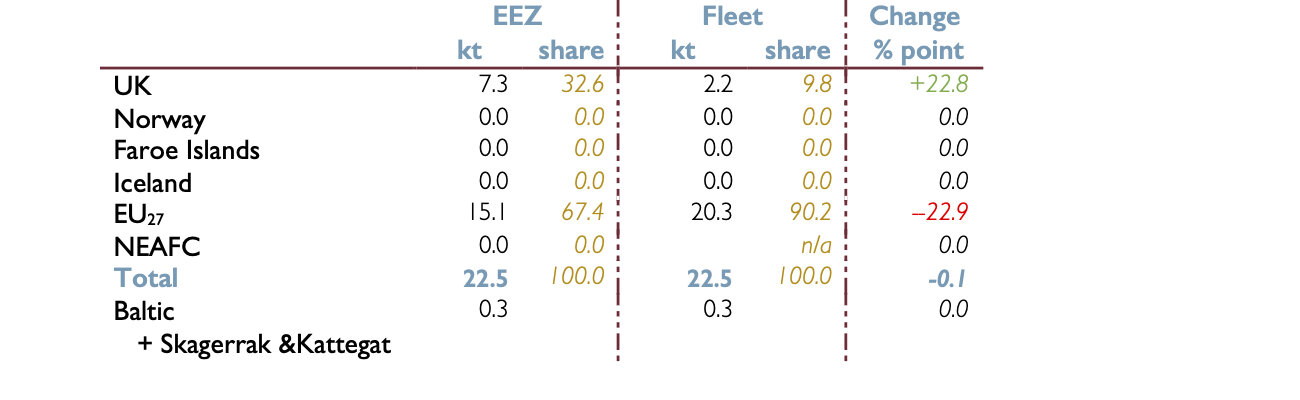

Table 1: Plaice landings from the NE Atlantic by EEZ and fleet

Faroe Islands: FI database does not specify location fish caught, all FI fleet landings assigned to FI EEZ. In reality some FI fleet landings might be from outside FI EZZ, in which case the FI EEZ figure will be lower and others correspondingly higher

The Norwegian database does not have separate entries for any flatfish other than Greenland Halibut.

The “Other flatfish” entry averages 8,768 tonnes for the years in question. Average catches from the Norwegian EEZ were 7,647 tonnes, 841 tonnes from the EU EEZ, 3 tonnes from FI and 1 from Icelandic EEZ

87% of Norwegian “Other flatfish” were landed from the Norwegian EEZ, 9.6% from the EU EEZ and virtually none from the FI and Icelandic EEZs

The species breakdown is unknown but this entry sets a ceiling for possible Norwegian fleet landings of 8.8 kt, with 7.6 kt from the Norwegian EEZ and 0.8 from the EU. In reality, since this entry includes a number of species, the figure for any individual species, such the five considered in this article, would be substantially lower.

The above notes regarding the Norwegian database apply to all five species in this article.

NEAFC: in reality landings from NEAFC would be landed by a national fleet but which fleet would be by agreement between parties to NEAFC. UK currently party to NEAFC through membership of EU. Post EU departure?

Plaice is the flatfish caught in the greatest quantities but it is also a relatively low value one. Over half of the Plaice landed from the NE Atlantic is landed from the EU27 EEZ. Nevertheless, the quotas allocated to the EU27 have allowed it to land more than its share of the resource.

If some of the 841 tonnes of ‘Other flatfish’ landed by the Norwegian fleet from the EU EEZ was Plaice then not only would Norwegian fleet landings and share not be zero but the landings and shares from other EEZs would be increased and the consequent reduction in UK and EU27 landings and shares would be correspondingly reduced.

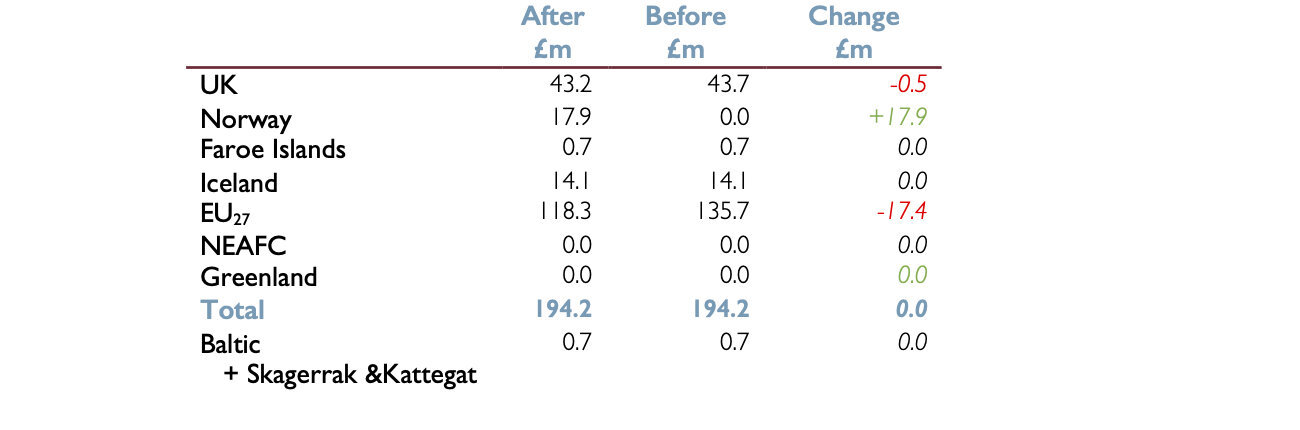

Table 2: Value of Plaice landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £1,820.00 /tonne

LEMON SOLE

Table 3: Lemon Sole landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

Faroe Islands: FI database does not specify location fish caught, all FI fleet landings assigned to FI EEZ. In reality some FI fleet landings might be from outside FI EZZ, in which case the FI EEZ figure will be lower and others correspondingly high.

Landed in much smaller quantities than Plaice, but higher in value, Lemon Sole is another species for which the EU27 has awarded itself a disproportionate share. A redistribution based on resource share would see the UK and the EU27swap places in terms of Lemon Sole landings.

Table 4: Value of Lemon Sole landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £4,707.00 /tonne

COMMON SOLE

Table 5: Common Sole landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Icelandic and Faroe Islands databases do not have a separate entry for Common Sole. In the case of Iceland, there is an “Other flatfish” entry. This average 222 tonnes for the years in question; all landed from the Icelandic EEZ. Icelandic landings would therefore have no impact on the redistribution.

The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Common Sole landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Common Sole from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27.

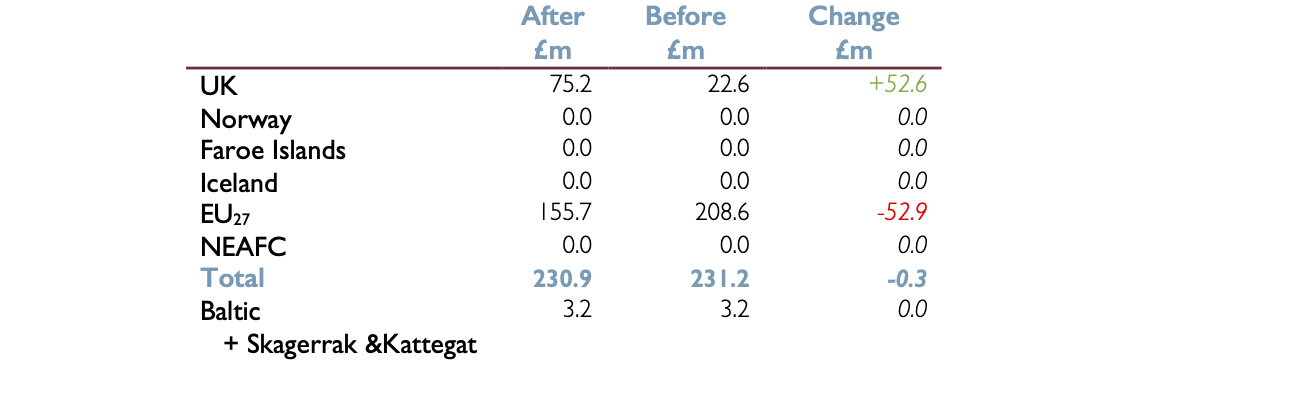

Roughly two thirds of Common Sole are landed are landed from the EU27, which means that post-redistribution the EU27 continues to land the bulk of Common Sole in the NE Atlantic. However, the UK receives substantial additional share (22.8 percentage points) to take its share from just 9.8% to the 32.6% landed from its EEZ; and this increase in share combined with absolute quantities that are several times those for Lemon Sole and a value that is getting on for six times that of Plaice means the potential gain to the UK is in excess of £50 million.

Table 6: Value of Common Sole landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £10,295.00 /tonne

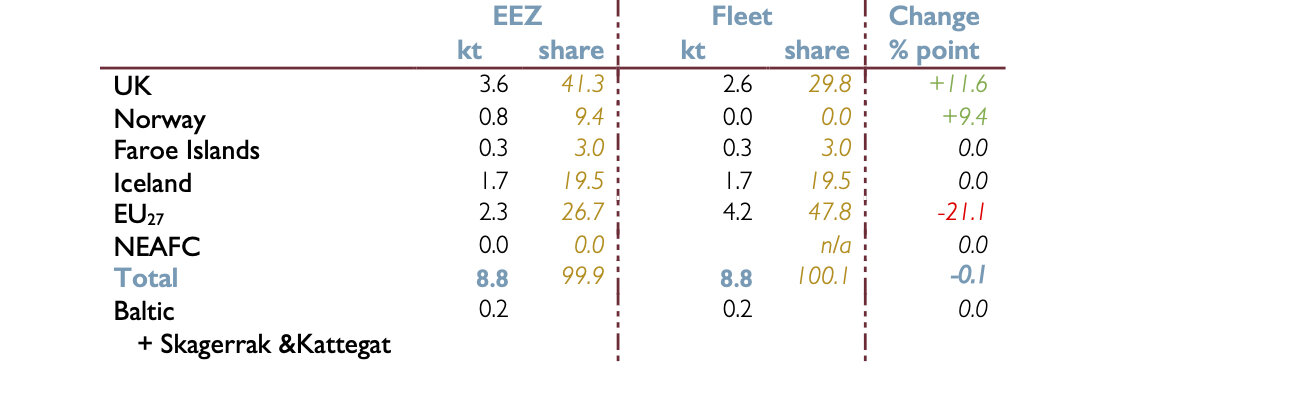

TURBOT

Table 7: Turbot landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Icelandic and Faroe Islands databases do not have a separate entry for Turbot either. In the case of Iceland, there is an “Other flatfish” entry. This average 222 tonnes for the years in question; all landed from the Icelandic EEZ. Icelandic landings would therefore have no impact on the redistribution.

The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Turbot landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Turbot from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27

Another species where a redistribution based on resource share would result in the UK receiving substantial additional share, although the EU27 EEZ would continue to be the dominant source of Turbot and its fleet would continue to land the bulk of the catch, albeit not a disproportionate share as at present.

Although the absolute tonnages of Turbot landed are small and the UK’s potential gain is just 0.5 kt, the high value of Turbot means that even half a kilotonne still yields an extra £5 million.

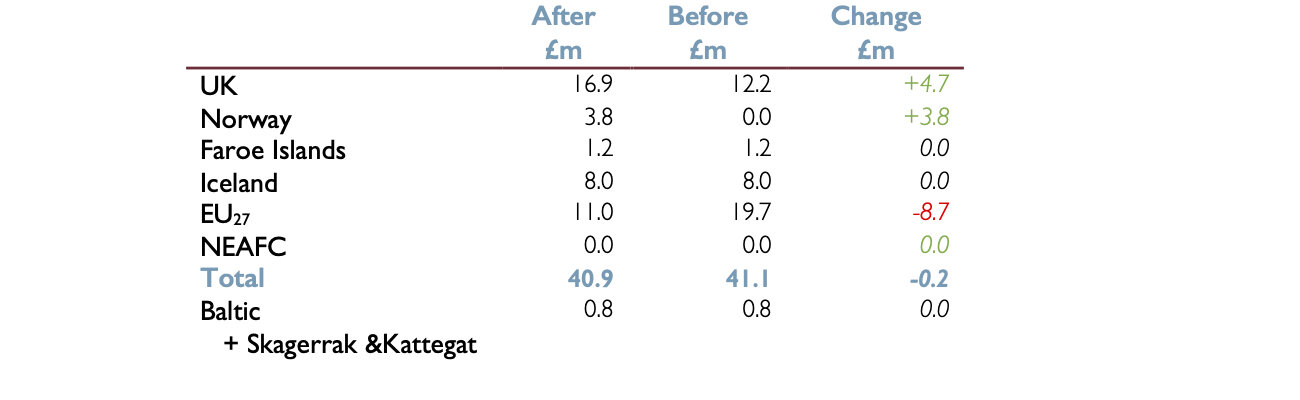

Table 8: Value of Turbot landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £10,513.00/tonne

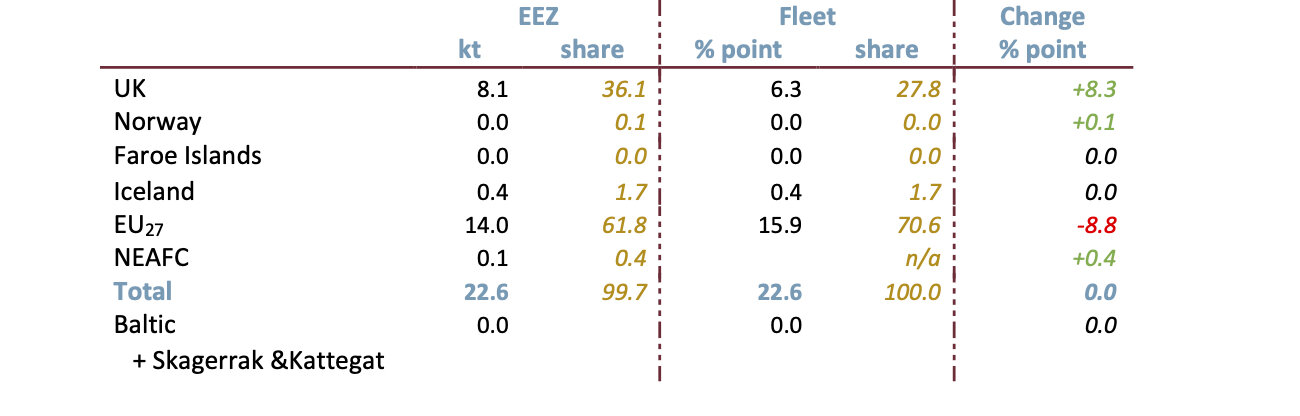

MEGRIMS

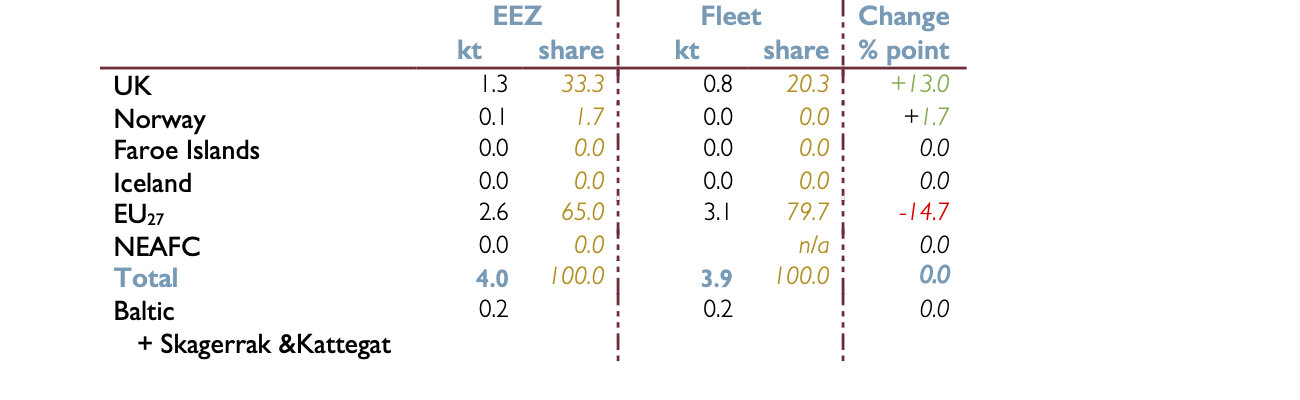

Table 9: Megrims landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Faroe Islands database does not have a separate entry for Megrims either. The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Megrims landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Megrims from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27

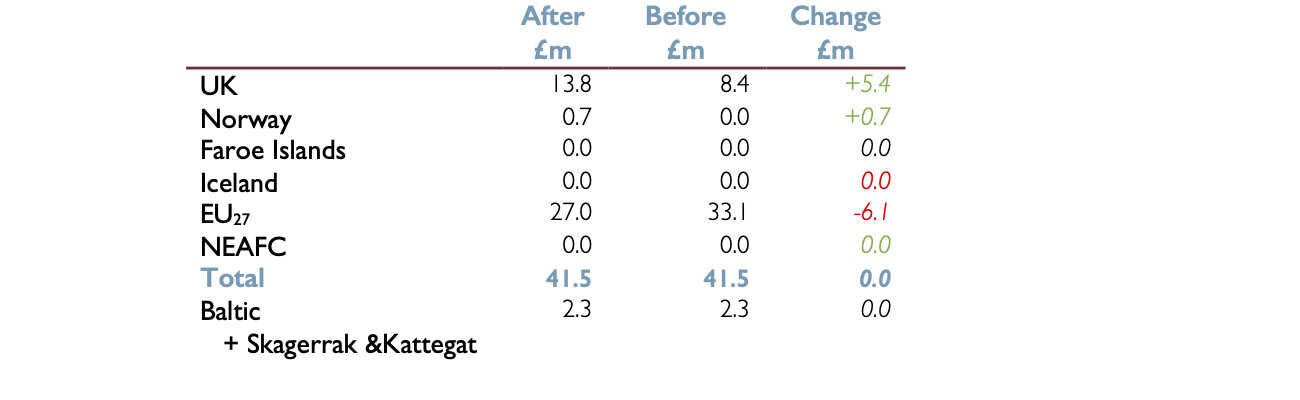

Landed in similar quantities to Lemon Sole but closer in value to Plaice, Megrim is another flatfish that is mainly landed from the EU27 EEZ but for which the UK’s current quotas does not reflect its share of the resource. Following a redistribution, UK landings might rise by a little over a quarter (8.3 percentage points) and bring in another £5 million.

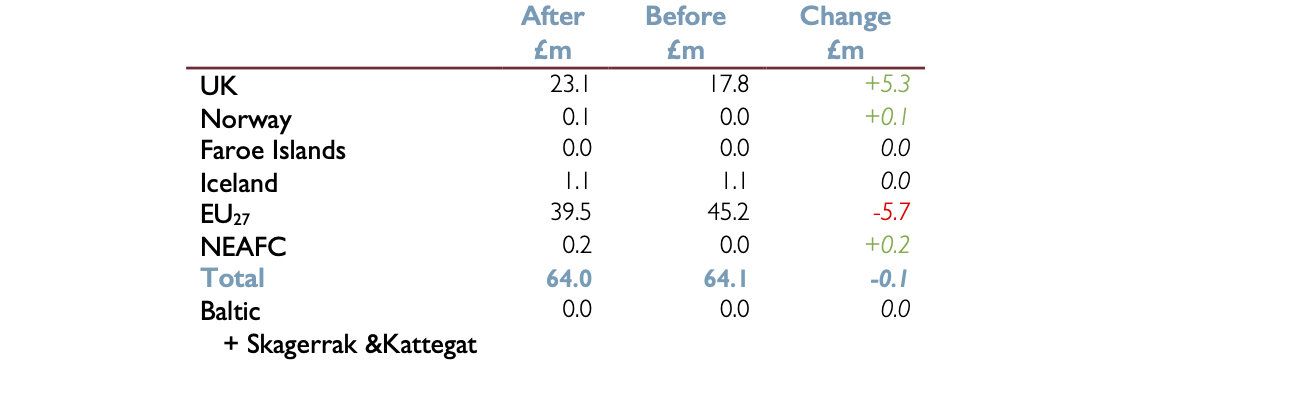

Table 10: Value of Megrims landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £2,833.00 /tonne*

*Defra 2017 prices

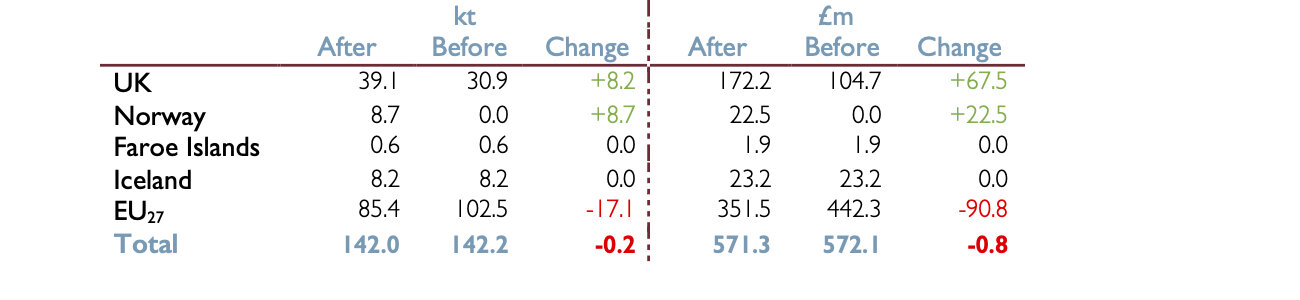

SUMMARY

To sum up the potential changes for these five species, Table 11 presents the overall tonnages and values of landings and how they might change if overall landings in future matched the average for 2010-16.

This assumption might well of course not hold good; and there are further uncertainties given the absence of data for some species and countries, the lack of geographical precision of some databases, how landings from international waters might be handled and the arbitrary use of UK 2018 prices as the basis for values, as has been highlighted above in the small print. Table 11 should therefore be viewed as an indicator of the direction of travel rather than a precise forecast.

Table 11: Summary

See note on Norwegian database in Plaice entry.

Note, the apparent overall loss of tonnage and value is more apparent than real, and relates to landings from NEAFC regulated international waters. In reality these fish would be landed; the question is by whom.

Flatfish are the EU27’s strong suit, with the EU27 EEZ accounting for roughly 60% of NE Atlantic landings of these five species. Nevertheless, as a result of the fact that EU27 landings during the period being considered were well in excess of its share of the resource, even here the EU27’s share would fall back following a redistribution.

Only 1 kilotonne of these five species is landed from the private EU27 lake that is the Baltic, Skagerrak and Baltic, so the EU27 would not be able to turn to it to buffer the impact of reduced share in the NE Atlantic.

Although the tonnages involved are much lower than for the species considered in the previous two articles, the high value of Common Sole and the extent to which the UK’s share would be adjusted means that the financial gain to the UK resulting from a redistribution of fishing opportunities for these five species exceeds that for the previous five.

Subscribe to our tea-time newsletter here, and follow us on Twitter here and facebook here.

After a first degree in zoology followed by research in developmental genetics, Neil Stratton worked for a number of European publishers before beginning an analysis of European fish landings with the think tank EH99 in the spring of 2018. The recently published report Fair Shares for All is based on this analysis.

Tuesday, 23 June 2020

Cornish Sardine season to start soon!

Beam trawler AA and the netter Ygraine with 50 boxes of hake along with plenty of quality monk and flats from the beam trawler St Georges landed to the market this morning...

while the sight of two ring netters brought up to dry out on the hard for work under the waterline anti-fouling are a sure sign that this year's Cornish sardine season is about to kick off...

no such luck for the stern trawler Spirited Lady as her replacement Volvo Penta main engine arrives on the quayside...

a few hours later and the tide has hardly dropped, Jason is already hard at work scrubbing off the weed below the waterline!

Government suffers heavy defeat on post-Brexit fishing policy as Lords push for more environmental protection

The Government has been heavily defeated in the Lords over demands to put environmental sustainability at the heart of post-Brexit fishing policy. Peers backed a cross-party amendment to the Fisheries Bill aimed at making this the prime objective to prevent over-fishing and damage to the marine environment. The Lords approved the amendment by 310 votes to 251, majority 59, in the report stage debate on the legislation and peers voted remotely and in Parliament.

The Bill enables the UK to become an independent coastal state post-Brexit, with foreign fishing boats barred from fishing in UK waters unless licensed to do so. But independent crossbencher Lord Krebs said that, as currently drafted, it did not guarantee the protection of fish stocks and the wider marine environment.

Take back control: A fisherman protests against an earlier Brexit withdrawal agreement(PA) To be absolutely sure the Bill “does what it claims to say on the tin, let’s get the commitment to protecting the natural environment written into it,” he said. Lord Krebs, a former chairman of the Food Standards Agency, said whenever there was a trade-off between short-term economic and employment considerations and long-term environmental sustainability, short-term factors nearly always won.

The Bill enables the UK to become an independent coastal state post-Brexit, with foreign fishing boats barred from fishing in UK waters unless licensed to do so. But independent crossbencher Lord Krebs said that, as currently drafted, it did not guarantee the protection of fish stocks and the wider marine environment.

Take back control: A fisherman protests against an earlier Brexit withdrawal agreement(PA) To be absolutely sure the Bill “does what it claims to say on the tin, let’s get the commitment to protecting the natural environment written into it,” he said. Lord Krebs, a former chairman of the Food Standards Agency, said whenever there was a trade-off between short-term economic and employment considerations and long-term environmental sustainability, short-term factors nearly always won.

“This is what has led to over-fishing and long-term damage to the marine environment in many of the world’s fisheries.” He said this was Parliament’s “huge chance to get the management of our fisheries on a genuinely sustainable footing and avoid the mistakes of the past”.

Backing the move for the Opposition, Baroness Jones of Whitchurch said sustainability of Britain’s fishing stock must be the “number one priority”. Lady Jones said: “It leaves behind the deals and the compromises that were an inevitable part of the common fisheries policy and will put our fisheries on more long-term assured footing, with fish stocks to fish for generations to come.”

But Environment, Food and Rural Affairs minister Lord Gardiner of Kimble warned the amendment would undermine the Bill’s carefully balanced approach to sustainability. Lord Gardiner said peers were all seeking the same thing – a “vibrant and sustainable fishing industry with a greatly improved marine environment”.

The industry could only be viable if it was environmentally sustainable and this was why the Bill gave equal weight to environmental, social and economic considerations, he added. He said the amendment would create a “hierarchy” of objectives and mean that in any circumstances “short-term environmental considerations would need to override even critical economic and social needs”.

But Environment, Food and Rural Affairs minister Lord Gardiner of Kimble warned the amendment would undermine the Bill’s carefully balanced approach to sustainability. Lord Gardiner said peers were all seeking the same thing – a “vibrant and sustainable fishing industry with a greatly improved marine environment”.

The industry could only be viable if it was environmentally sustainable and this was why the Bill gave equal weight to environmental, social and economic considerations, he added. He said the amendment would create a “hierarchy” of objectives and mean that in any circumstances “short-term environmental considerations would need to override even critical economic and social needs”.

Lord Gardiner warned the change could have a severe impact on parts of the UK fishing industry and could lead to the closure of mixed fisheries where most fish stocks were at a sustainable level but some were in recovery.

Subscribe to:

Comments (Atom)