By Neil Stratton

THIS ARTICLE, the third in a series that considers – how fish landings might look if the major fleets fishing in the NE Atlantic landed a share of the overall harvest that matched the share taken from the corresponding EEZ – examines five species of flatfish: Plaice, Lemon Sole, Common Sole, Turbot and Megrims (strictly speaking, Megrims is a genus).

The first article included general notes about data sources, methodology and the caveat that the following analyses do not assume any particular form of fisheries agreement but merely provide an indication of how shares would change if such an agreement or agreements matched give to take. These continue to apply.

So, without further ado let’s start with Plaice.

PLAICE

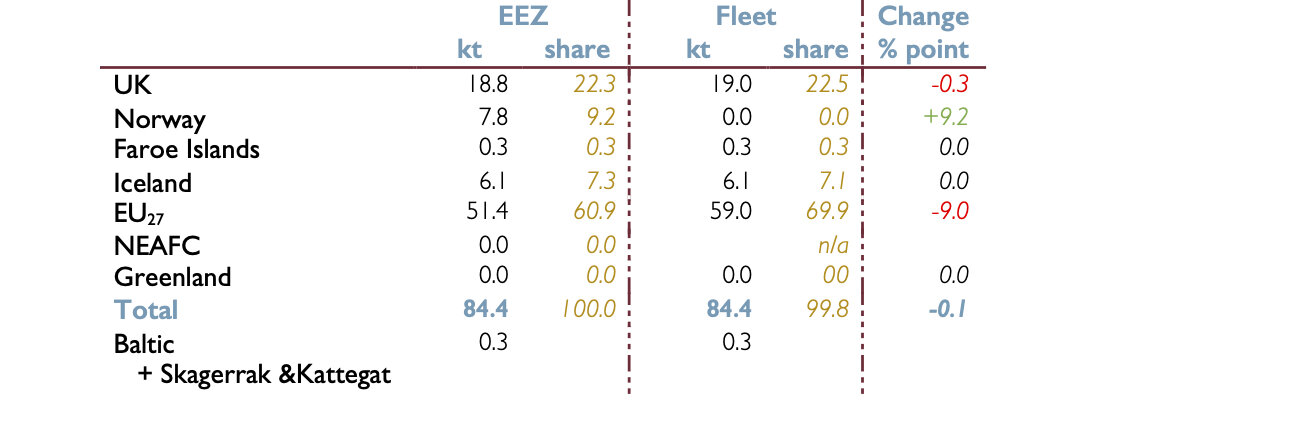

Table 1: Plaice landings from the NE Atlantic by EEZ and fleet

Faroe Islands: FI database does not specify location fish caught, all FI fleet landings assigned to FI EEZ. In reality some FI fleet landings might be from outside FI EZZ, in which case the FI EEZ figure will be lower and others correspondingly higher

The Norwegian database does not have separate entries for any flatfish other than Greenland Halibut.

The “Other flatfish” entry averages 8,768 tonnes for the years in question. Average catches from the Norwegian EEZ were 7,647 tonnes, 841 tonnes from the EU EEZ, 3 tonnes from FI and 1 from Icelandic EEZ

87% of Norwegian “Other flatfish” were landed from the Norwegian EEZ, 9.6% from the EU EEZ and virtually none from the FI and Icelandic EEZs

The species breakdown is unknown but this entry sets a ceiling for possible Norwegian fleet landings of 8.8 kt, with 7.6 kt from the Norwegian EEZ and 0.8 from the EU. In reality, since this entry includes a number of species, the figure for any individual species, such the five considered in this article, would be substantially lower.

The above notes regarding the Norwegian database apply to all five species in this article.

NEAFC: in reality landings from NEAFC would be landed by a national fleet but which fleet would be by agreement between parties to NEAFC. UK currently party to NEAFC through membership of EU. Post EU departure?

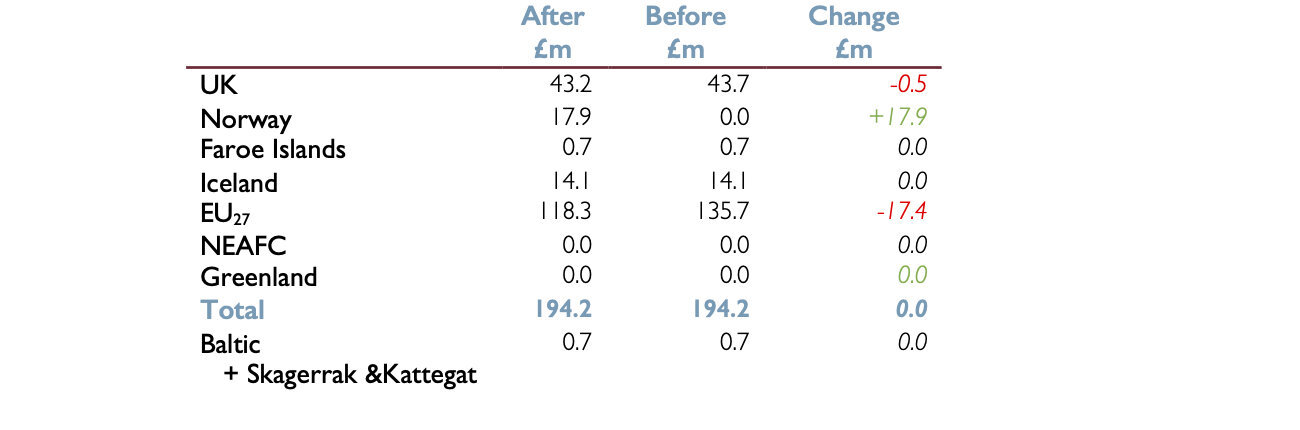

Plaice is the flatfish caught in the greatest quantities but it is also a relatively low value one. Over half of the Plaice landed from the NE Atlantic is landed from the EU27 EEZ. Nevertheless, the quotas allocated to the EU27 have allowed it to land more than its share of the resource.

If some of the 841 tonnes of ‘Other flatfish’ landed by the Norwegian fleet from the EU EEZ was Plaice then not only would Norwegian fleet landings and share not be zero but the landings and shares from other EEZs would be increased and the consequent reduction in UK and EU27 landings and shares would be correspondingly reduced.

Table 2: Value of Plaice landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £1,820.00 /tonne

LEMON SOLE

Table 3: Lemon Sole landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

Faroe Islands: FI database does not specify location fish caught, all FI fleet landings assigned to FI EEZ. In reality some FI fleet landings might be from outside FI EZZ, in which case the FI EEZ figure will be lower and others correspondingly high.

Landed in much smaller quantities than Plaice, but higher in value, Lemon Sole is another species for which the EU27 has awarded itself a disproportionate share. A redistribution based on resource share would see the UK and the EU27swap places in terms of Lemon Sole landings.

Table 4: Value of Lemon Sole landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £4,707.00 /tonne

COMMON SOLE

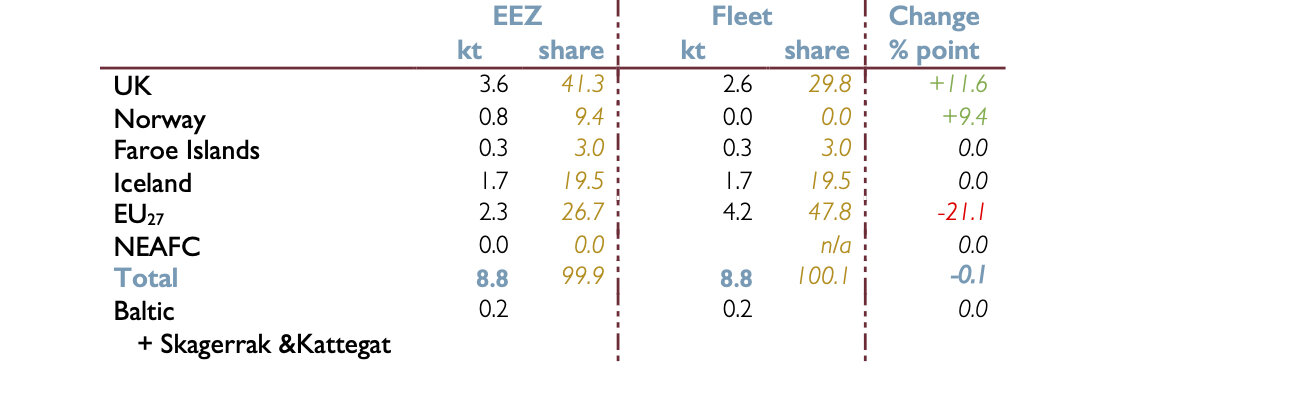

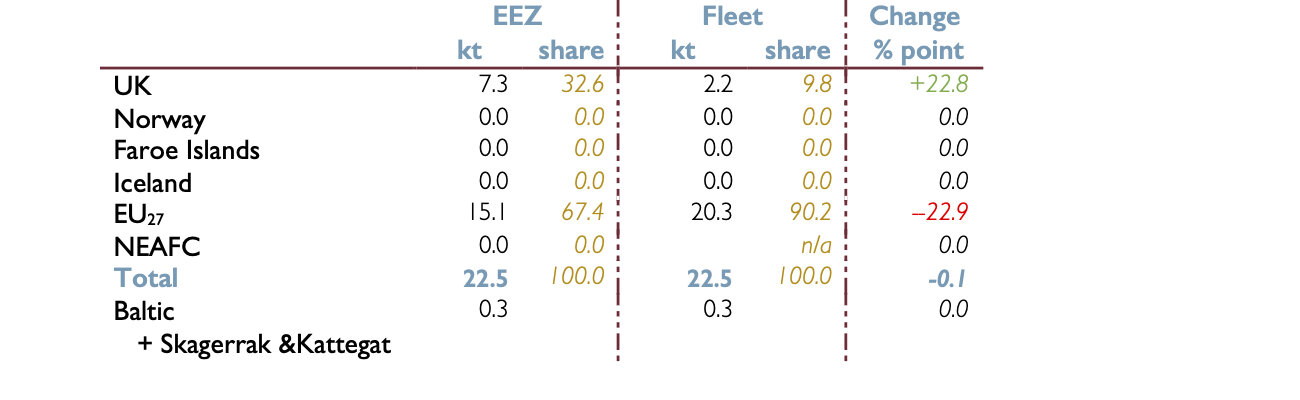

Table 5: Common Sole landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Icelandic and Faroe Islands databases do not have a separate entry for Common Sole. In the case of Iceland, there is an “Other flatfish” entry. This average 222 tonnes for the years in question; all landed from the Icelandic EEZ. Icelandic landings would therefore have no impact on the redistribution.

The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Common Sole landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Common Sole from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27.

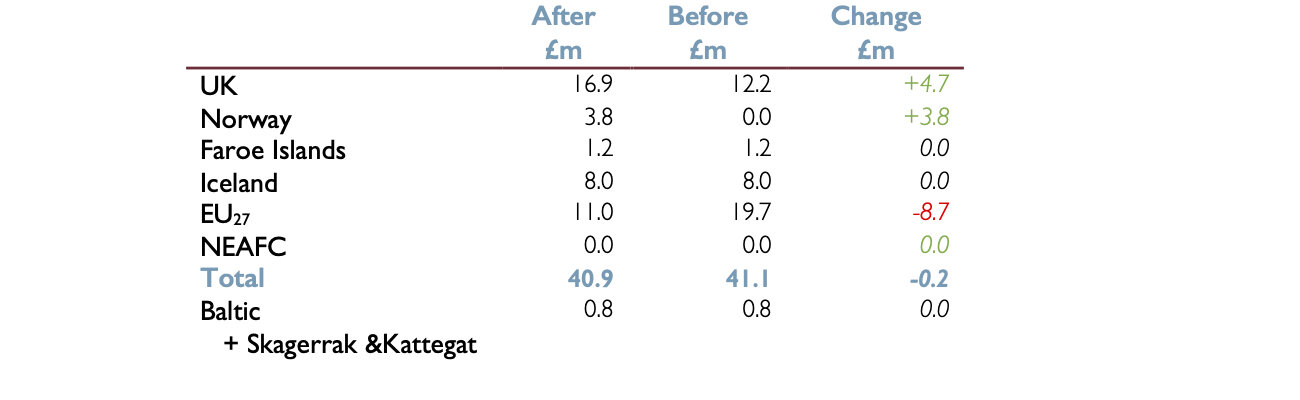

Roughly two thirds of Common Sole are landed are landed from the EU27, which means that post-redistribution the EU27 continues to land the bulk of Common Sole in the NE Atlantic. However, the UK receives substantial additional share (22.8 percentage points) to take its share from just 9.8% to the 32.6% landed from its EEZ; and this increase in share combined with absolute quantities that are several times those for Lemon Sole and a value that is getting on for six times that of Plaice means the potential gain to the UK is in excess of £50 million.

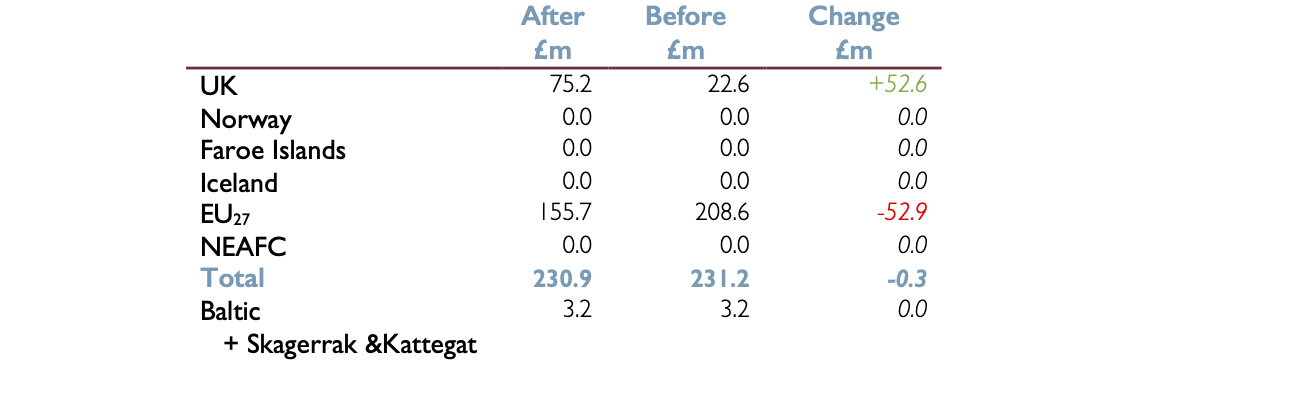

Table 6: Value of Common Sole landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £10,295.00 /tonne

TURBOT

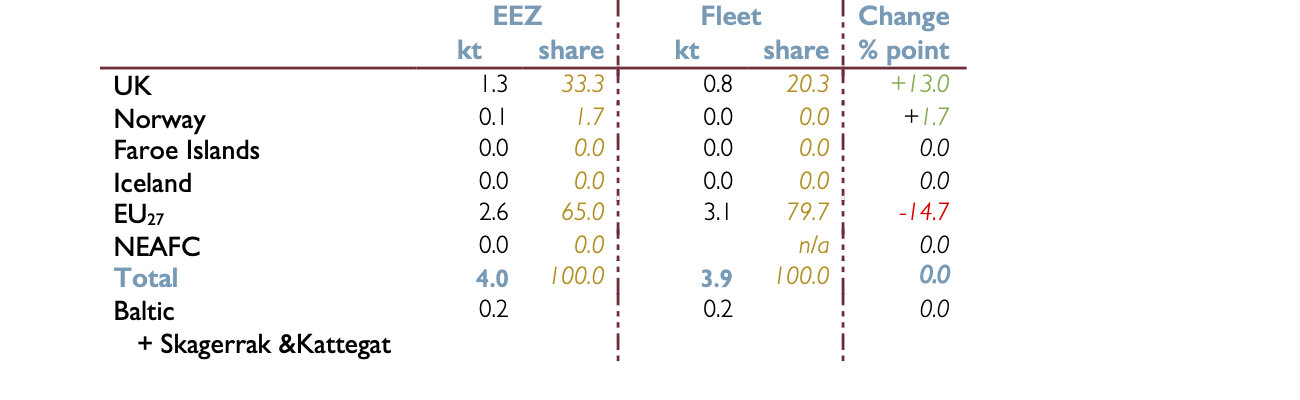

Table 7: Turbot landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Icelandic and Faroe Islands databases do not have a separate entry for Turbot either. In the case of Iceland, there is an “Other flatfish” entry. This average 222 tonnes for the years in question; all landed from the Icelandic EEZ. Icelandic landings would therefore have no impact on the redistribution.

The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Turbot landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Turbot from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27

Another species where a redistribution based on resource share would result in the UK receiving substantial additional share, although the EU27 EEZ would continue to be the dominant source of Turbot and its fleet would continue to land the bulk of the catch, albeit not a disproportionate share as at present.

Although the absolute tonnages of Turbot landed are small and the UK’s potential gain is just 0.5 kt, the high value of Turbot means that even half a kilotonne still yields an extra £5 million.

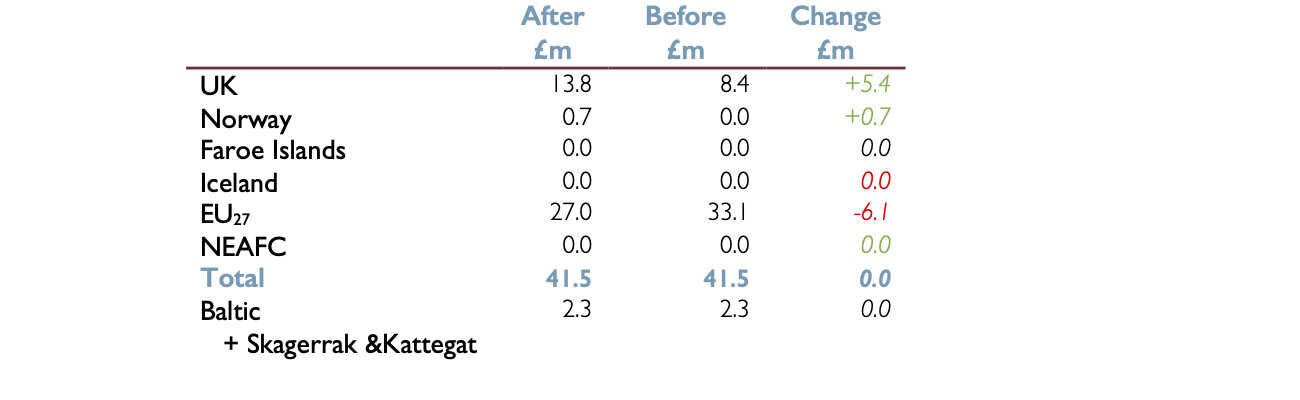

Table 8: Value of Turbot landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £10,513.00/tonne

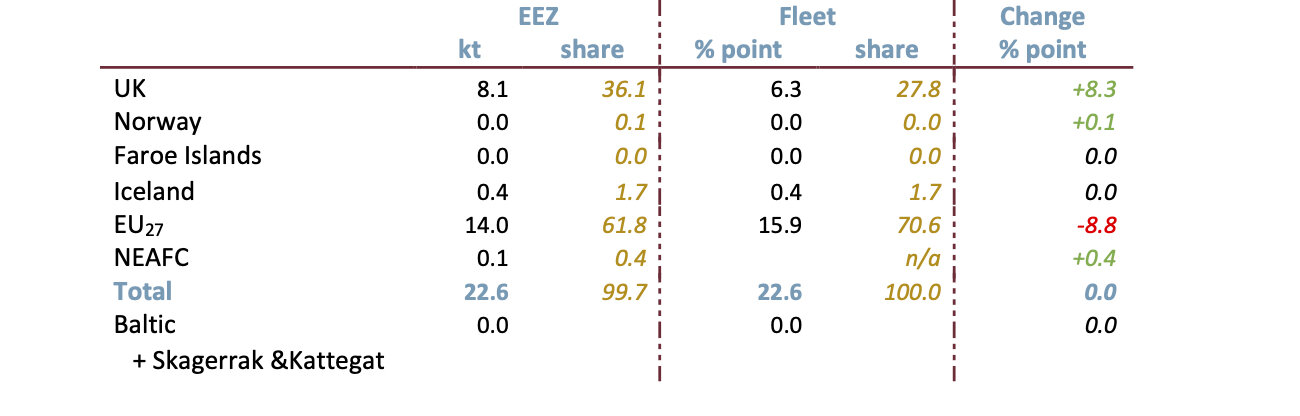

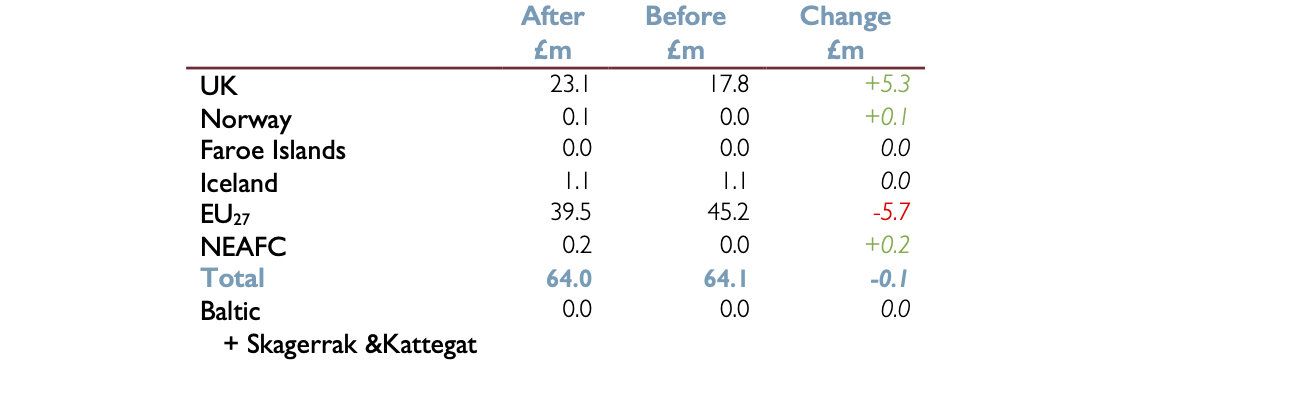

MEGRIMS

Table 9: Megrims landings from the NE Atlantic by EEZ and fleet

See note on Norwegian database in Plaice entry.

The Faroe Islands database does not have a separate entry for Megrims either. The Faroe Islands has no “Other flatfish” entry but it does have an “Other” fish entry, this averages 2,088.9 tonnes for the years for which FI figures are available. FI Megrims landings could not therefore exceed 2.1 kt; in reality they are likely to be much less.

EU27 and UK landings of Megrims from the FI and Norwegian EEZs are close to zero and are zero for the Icelandic EEZ; this coupled with the lack of separate entries in the Norwegian and FI databases suggests FI and Norwegian landings are ‘modest’.

It is not therefore possible to model how landings might be redistributed for all NE Atlantic fleets and EEZs and the above table really looks at just the UK and the EU27

Landed in similar quantities to Lemon Sole but closer in value to Plaice, Megrim is another flatfish that is mainly landed from the EU27 EEZ but for which the UK’s current quotas does not reflect its share of the resource. Following a redistribution, UK landings might rise by a little over a quarter (8.3 percentage points) and bring in another £5 million.

Table 10: Value of Megrims landings from the NE Atlantic by EEZ and fleet

Before and after a possible redistribution @ £2,833.00 /tonne*

*Defra 2017 prices

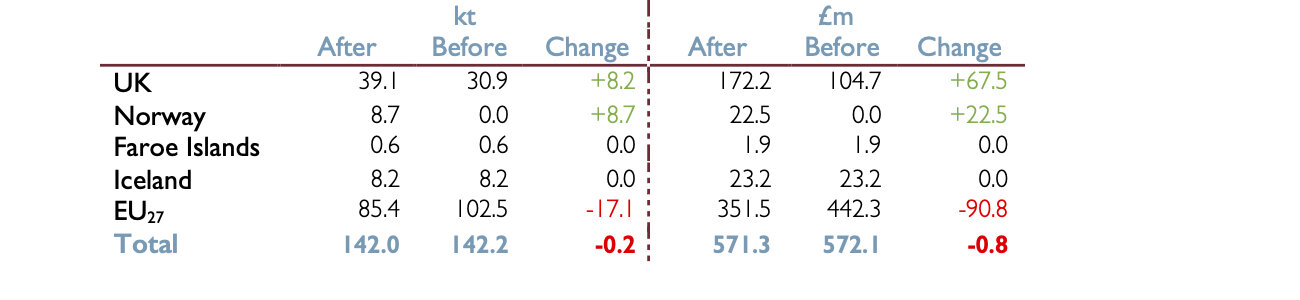

SUMMARY

To sum up the potential changes for these five species, Table 11 presents the overall tonnages and values of landings and how they might change if overall landings in future matched the average for 2010-16.

This assumption might well of course not hold good; and there are further uncertainties given the absence of data for some species and countries, the lack of geographical precision of some databases, how landings from international waters might be handled and the arbitrary use of UK 2018 prices as the basis for values, as has been highlighted above in the small print. Table 11 should therefore be viewed as an indicator of the direction of travel rather than a precise forecast.

Table 11: Summary

See note on Norwegian database in Plaice entry.

Note, the apparent overall loss of tonnage and value is more apparent than real, and relates to landings from NEAFC regulated international waters. In reality these fish would be landed; the question is by whom.

Flatfish are the EU27’s strong suit, with the EU27 EEZ accounting for roughly 60% of NE Atlantic landings of these five species. Nevertheless, as a result of the fact that EU27 landings during the period being considered were well in excess of its share of the resource, even here the EU27’s share would fall back following a redistribution.

Only 1 kilotonne of these five species is landed from the private EU27 lake that is the Baltic, Skagerrak and Baltic, so the EU27 would not be able to turn to it to buffer the impact of reduced share in the NE Atlantic.

Although the tonnages involved are much lower than for the species considered in the previous two articles, the high value of Common Sole and the extent to which the UK’s share would be adjusted means that the financial gain to the UK resulting from a redistribution of fishing opportunities for these five species exceeds that for the previous five.

Subscribe to our tea-time newsletter here, and follow us on Twitter here and facebook here.

After a first degree in zoology followed by research in developmental genetics, Neil Stratton worked for a number of European publishers before beginning an analysis of European fish landings with the think tank EH99 in the spring of 2018. The recently published report Fair Shares for All is based on this analysis.